‘Corporate tax avoidance’ tops UK public’s list of concerns for 10th consecutive year, with disquiet at record high

‘Corporate tax avoidance’ tops list of concerns, with disquiet at record high

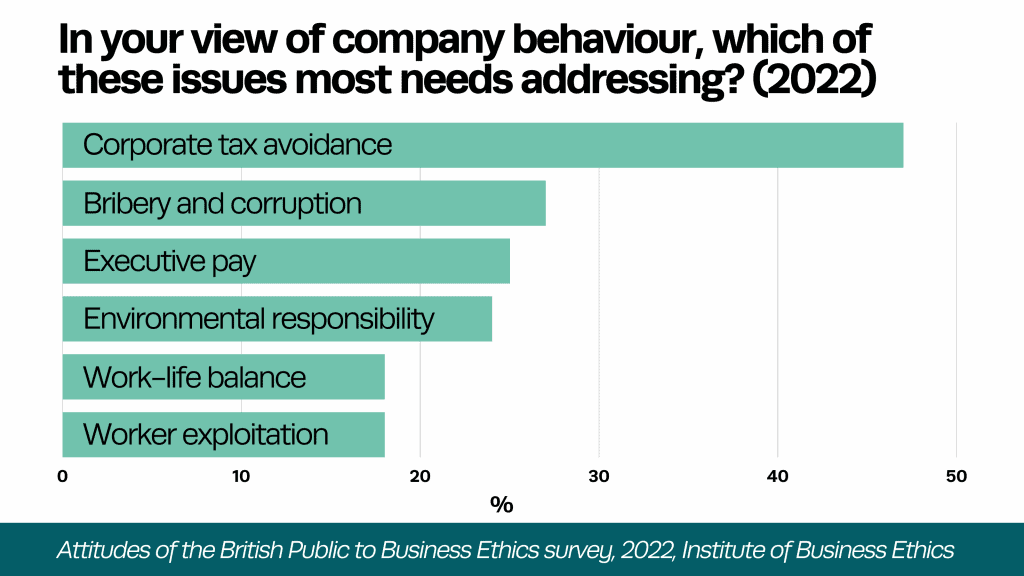

‘Corporate tax avoidance’ has topped the UK public’s list of concerns for an astounding tenth consecutive year. Moreover, the level of disquiet is at a record high, with 47% citing it among their top three ethical concerns when questioned in May 2022 as part of the Institute for Business Ethics (IBE) annual survey.

These findings are in line with our own recent Fair Tax Foundation polling, which found that:

- three quarters of respondents would rather shop with (74%) or work for (75%) businesses that can prove that they are paying their fair share of tax;

- nearly four in five (77%) believe all companies, whatever their size, should have to publicly disclose the taxes that they do or don’t pay in the UK;

- over two thirds (66%) believe the Government and local councils should consider a company’s ethics and how they pay their tax, as well as value for money and quality of service provided, when awarding contracts to companies,

It would appear that the unprecedented national discourse over the last twelve months on the need for the UK to stop leading the race to the bottom among major economies on corporation tax has struck a nerve as never before. In particular, the Government’s newfound support for both a global minimum tax (to curtail profit shifting to tax havens by multinationals) and an increase in the UK’s headline rate (from 19 to 25%) would be landmark developments should they materialise in 2023, as recently announced.

Also noteworthy is that ‘bribery and corruption’ is now the second most cited concern for the first time in twenty years of polling by the IBE. This is likely a consequence of the increased general awareness of the UK as a global hub for dirty money and corruption, following Russia’s invasion of Ukraine and the exposure of various connected kleptocrats and their ill-gotten illicit wealth. Together, with prominent coverage of the substantial fraud that is being suffered by the UK’s covid support schemes.

‘Generation gap’ disappears

In previous research, by both the IBE and Fair Tax Foundation, there has been a significant difference in the levels of concern that younger and older adults have expressed around corporate tax avoidance. Make no mistake, all age groups express substantial levels of concern, but older demographics have previously expressed significantly heightened disquiet – in some cases our research has found as much thirty-four percentage points of difference!

We’ve racked our brains as to why this might be. Is it down to older people being more reliant on public services (such as the NHS) and valuing them more? Or, are younger adults so wedded to the tech of tax dodgers such as Apple and Amazon that they become ethically compromised? Either way, the IBE’s latest research has found that this ‘generation gap’ has all but disappeared – what was a twenty percentage point difference between 18-34 years and 55+ years is now an insignificant four percentage point gap. It will be fascinating to see if our own research picks this up in future cycles.

Mandate for action

So, what does this all mean? Well, for one thing, it’s pretty clear that there is a rock-solid mandate for politicians of all political persuasions to take action and clamp down on corporate tax avoidance. The issue has real substance as well. Aggressive tax avoidance negatively distorts national economies and undermines the ability of business to compete fairly, both domestically and internationally. Recent research has found that close to 40% of multinational profits (some US$950bn) are artificially shifted to tax havens each year, leading to a US$240bn reduction in corporate income tax revenue. Within this, the UK was found to suffer a staggering US$120bn of profit shifting, leading to an estimated $23bn reduction in corporation tax revenues – which equates to £17bn of missing tax, or 28% of what is collected. HMRC may claim that corporate tax avoidance costs the UK just £600mn per annum in terms of lost revenue, but this estimate is equally self-serving and laughable, as set out by our CEO in a recent twitter thread.

But more than this, there is a consensus that businesses should make a meaningful tax contribution, and pay corporation tax where they generate value and surplus. As previously noted, the UK Government’s newfound support for both a global minimum tax (to curtail profit shifting to tax havens by multinationals) and an increase in the UK’s headline rate (from 19 to 25%) is to be applauded. Currently, the UK has the lowest corporation tax of any major economy on the planet. Even when it rises to 25%, it will still be the lowest among G7 nations.

Worryingly, there is substantial media speculation suggesting that both measures may be curtailed at the behest of Prime Minister, Boris Johnson before they ever come into being. This would swim against the current of both public and business sentiment. The majority of UK “big business” is not out there actively lobbying for a cut in Corporation Tax. They recognise that they need to do their bit and contribute to vital public services. They want to compete on an equal footing in the UK and abroad, and not cheat the system or secure unfair advantage. They trust their own capabilities to thrive on a level playing field.

There is little evidence to support the idea that cuts to the headline rate of corporation tax leads to greater investment and therefore greater profits and therefore greater tax receipts – the so-called Laffer Curve. This is hard right dogma. The UK Chancellor, Rishi Sunak, to his credit recognises this. It is noteworthy that when Donald Trump slashed US Corporation Tax rate (promising the usual Laffer Curve nonsense of increased tax take) they saw no investment surge and tax revenues fell. The only upsurge was in corporate share buybacks as many businesses were suddenly swimming in cash.

We would urge that the UK stay the course and substantially progress the corporation tax proposals announced and provide profitable business with a platform to provide fair and meaningful tax contribution.