Latest analysis of corporate compliance with EU pCbCR Directive: 60% of business perform well, but US and Swiss multinationals are laggards

Summary of findings

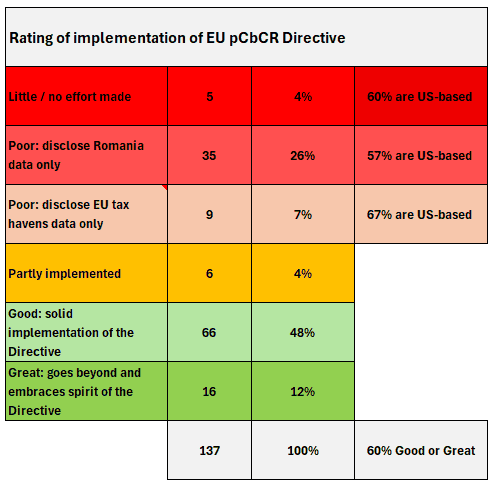

137 EU public Country-by-Country reports sourced and analysed. The most extensive analysis published globally to date, to the best of our knowledge.

-

- Almost two-thirds (60%) of corporate pCbCR reports are good, solid attempts to implement legislation driven by the EU pCbCR Directive.

- However, in 7% of instances, business have opted to confine disclosures to EU designated tax havens, and refuse to be transparent about their impact across EU Member States.

- Furthermore, a quarter of parent companies (26%) will not share CbCR data with their Romanian subsidiaries and are effectively refusing to implement the legislation.

- The frequency of good application of the EU pCbCR requirements was substantially above average among Japanese- and UK-headquartered business (at 75%). It was substantially lower than average among Swiss (44%) and US business (43%).

- A significant minority of business embraced the spirit as well as the letter of the legislation, and progressed full public country-by-country reporting and/or voluntarily progressed the EU pCbCR ahead of legislative requirements.

The following is an update on research presented on 10th June1, when the Fair Tax Foundation sourced and analysed a first batch of 75 tax transparency reports that emerged as a result of the EU’s public pCbCR Directive. All assessed reports are driven by either: i) mandatory capture of multinationals by Romania’s early implementation of the EU pCbCR Directive; or, ii) explicit, early voluntary implementation of the Directive by multinationals.2

We hope to update this research on a regular basis, and plan to make it freely available to all business that are involved in our Fair Tax Mark certification scheme and our Tax Responsibility and Transparency benchmarking index.3 If you would like to engage with us on this work please reach out to [email protected]

Background

The EU public Country-by-Country Reporting (pCbCR) Directive has begun to impact large multinationals around the world. The directive requires large multinational companies that have a substantial presence in Europe to publicly share key financial information on their operations in each EU Member State and a designated list of tax havens.4 In the main, the Directive will lead to major new corporate tax disclosures in 2026, based on 2025’s financial data. However, Romania opted to implement the EU Directive much earlier than other Member States, with data relating to 2023 starting to emerge at end 2024. We are now seeing the first EU pCbCR disclosures come to light.

An oddity in the way Romania has implemented the Directive means that only multinationals with significant operations in Romania, but that are headquartered outside of the EU, are impacted as yet – i.e., businesses with an ultimate parent entity in the US, Switzerland, Japan, the UK, etc.

We conducted extensive online searches to find these first EU pCbCR public reports and have identified 137 to date. There is no central repository of reports. Research was not as simple as might be hoped as the Romanian business register is not yet operational as a public repository of such information. Furthermore, there are no penalties in Romania for neglecting to implement the legislation as required. Which means, we suspect, that there are a sizeable minority of business who have simply opted to ‘ignore’ the legislation or are waiting to see how their competitors respond. For example, we have not, as would be expected, found returns from the likes of Amazon, IBM and Samsung. This needs to be borne in mind in the analysis that follows: whatever their rating, at the very least, all of the 137 companies identified as producing information on their website in connection with the EU pCbCR Directive have at least acknowledged its existence in some way.

Findings and ratings

The good news: the majority of business have embraced the EU pCbCR Directive fully

Almost two-thirds (60%) of the returns that are newly available are good, solid attempts to implement the EU pCbCR legislation.

This is to be warmly welcomed, with the businesses undertaking this deserving of applause. They have followed the letter of the law and are now ahead of many of their peers. This includes the likes of Natura (Brazil), Honda Motor (Japan), Colt Technology Services (US) and International Personal Finance (UK).

Many have gone further and embraced the spirit of the law and provided country-by-country data on a wider range of countries than is stipulated by regulations. Examples include GSK (UK), LG Electronics (South Korea), Adecco Group (Switzerland), Nippon Sheet Glass (Japan) and Sun Pharmaceutical (India).

We identified seven businesses that had explicitly implemented the EU pCbCR earlier than legally required. So, hats off to: SII Group (France), Vinci (France), Inter IKEA (Netherlands), Nilfisk (Denmark), Repsol (Spain), Allianz (Germany) and Havenbedrijf Rotterdam (Netherlands).5

The frequency of good application of the EU pCbCR requirements was substantially above average among Japanese- and UK-headquartered business (at 75%). It was substantially lower than the average among Swiss (43%) and US businesses (44%).

It was surprising to see that even businesses that robustly released hard data, did not provide accompanying narrative in their returns. Little or no meaningful context was provided in ‘section 5’ of the EU pCbCR returns of nearly every business examined – including a number that had a significant trading presence in Russia at the time, such as Philip Morris International (US). We expect this lack of narrative will prove to be problematic in the months and years to come. Without context and explanation, data may be misinterpreted and misunderstandings arise. A substantial minority of business did provide narrative, but usually in bespoke tax transparency reports. For best practice in this area is described at out our pCbCR Resources Hub.

The bad news

Less positively, in 7% of instances, business have opted to disclose activities in tax havens only. Examples, include Bristol Myers Squibb (US) and Ringier (Switzerland).

Worse still, in a further 26% of cases, Romanian subsidiaries have been ‘told’ by their parent company that they will not be provided (as a point of principle) with the information needed to disclose activity outside of Romania – i.e, the parent company is refusing to implement the legislation. This tactic is especially common among Swiss business (50% of whom deploy this tactic) and US business (36%). Examples include: Hitachi (Japan), Johnson & Johnson (US), Merck (US), Microsoft (US), Morningstar (US), Novartis (Switz), Proctor & Gamble (US) and SGS (Switzerland). Morningstar being on this list is something of a surprise given their ownership of Sustainalytics , who specialize in the provision of ESG research and corporate risk ratings.

Sectoral differences

It was noteworthy that the pharmaceuticals sector had a significantly below average rate of application: with just three of the nine companies (33%) showing solid implementation of the directive, whilst five (56%) opted for the ‘Romania only’ option. The automotive and food & beverages sectors also stood out as laggards, with just 38% and 44% showing solid implementation of the directive, respectively.

Technology was the largest sector for which reports were available, accounting for 18.5% of the sample. Just over half (52%) of the sector demonstrated good or great implementation of the directive, with a quarter (24%) restricting data disclosure to ‘Romania-only’.

Conversely, the industrials sector demonstrated above average levels of compliance and responsibility, as did chemicals, communications, consumer goods and manufacture.

The performance of the business & financial services sector is impacted by the fact that large financial institutions operating in Europe have needed to produce public country-by-country reports for some years, as per the Capital Requirements Directive IV, and are therefore exempt from the pCbCR Directive.6

Location of ultimate parent entity

As might be expected, companies head-quartered in the United States top the list of businesses captured by the legislation in Romania (41%), followed by Japan, Switzerland and the UK (at 12% each).

The near future

We can expect more late returns connected to Romania to emerge in the coming months. Beyond that, we should look to Croatia and Bulgaria next, where an earlier than average filing date also applies. More substantially, early reporting can also be anticipated for businesses filing in Spain, where the requirement is for pCbCR to be published within six months of the closing of the balance sheet, not the standard twelve months.

Comment

Paul Monaghan, Fair Tax Foundation, Chief Executive commented: “There is much to celebrate in our findings, but also causes for concern. The majority of multinationals that are impacted by the EU pCbCR Directive have implemented these new tax transparency rules with integrity and courage. Some have even taken the opportunity to go much further, and extend their reporting to all countries in which they operate and to other taxes. Others have opted to implement the directive earlier than required. On the other hand, many businesses, especially those based in the United States and Switzerland, have opted to do little or nothing. This is unfortunate, not least as robust implementation of the EU pCbCR is sure to become a prominent KPI of responsible tax conduct among investors and other stakeholders.”

Businesses wishing to get ahead of the curve are invited to visit our pCbCR Resource Hub, which includes a list of Fair Tax Mark certified exemplars of tax transparency.

Footnotes and references

- See “EU public Country-by-Country Reporting Directive takes early effect in Romania: implementation differs greatly across business“. ↩︎

- Romania’s early implementation of the EU pCbCR Directive impacts multinationals headquartered outside the EU that have a medium or large subsidiary – from financial years starting on or after 1st January 2023. Business that have demonstrated early voluntary implementation of the Directive account for seven of the 130 reports analysed. ↩︎

- We are reasonably confident that we have discovered the bulk of reports that have been published to date. Further reports are still emerging in connection with Romania for year ends after 31st December 2023, such as 31st March 2024, 31st May 2024 and 30th June 2024. Searches were undertaken in English and Romanian. Beyond Romania, we expect reports to start emerging in Croatia and Bulgaria toward end 2025. ↩︎

- Directive (EU) 2021/2101. Multinationals with an annual consolidated turnover of at least €750m. See our pCbCR Global Country Tracker for a list of EU and EEA States and the designated ‘tax havens’ (ie., the EU’s list of “non-cooperative tax jurisdictions”). ↩︎

- Many other businesses voluntarily already meet, or surpass the EU pCbCR requirements. Including a good number of Fair Tax Mark accredited businesses, such as Fortum (Finland), Iberdrola (Spain) and Mundys (Italy). However, they have not been including in this analysis as they do not explicitly claim that their reporting currently meets the EU pCbCR standard. ↩︎

- Article 89 of the Capital Requirements Directive (Directive 2013/36/EU or ‘CRD IV’) provides for country-by-country reporting by financial institutions, such as banks, building societies, other credit institutions and certain investment firms. CRD IV became law in 2013, with implementation by Member States required by 1 January 2014, and the first reporting from 30 June 2014. Disclosures include net banking income, earnings before tax, amount of taxes paid and the number of employees for each country where the bank has an affiliate. See https://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2013:176:0338:0436:EN:PDF ↩︎