Research reveals that multinationals are divided on tax transparency, with MNEs from the United States increasingly laggards

Just over half (56%) of the 190 corporate tax transparency reports published by large multinationals in connection with the EU Public Country-by-Country Reporting (pCbCR) Directive are good, solid attempts to be open and honest.

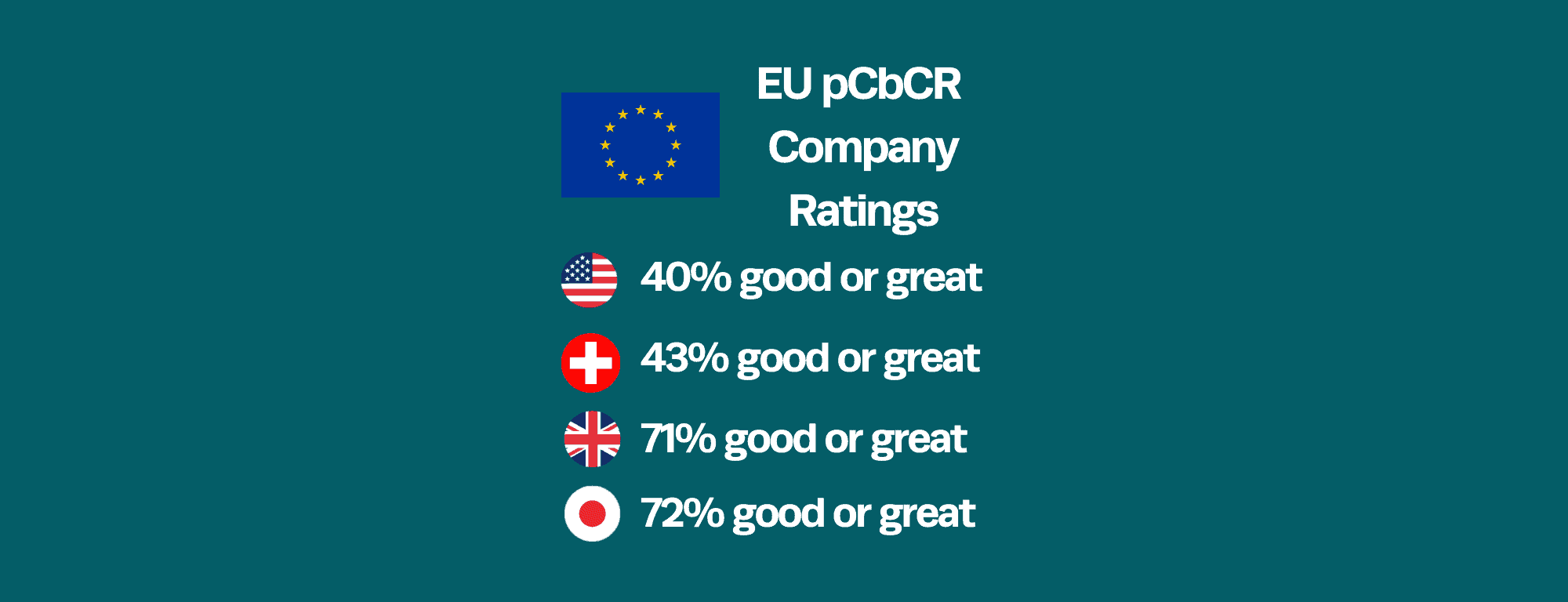

However, there are wide national variances. The frequency of good application of the EU pCbCR requirements was substantially above average among business headquartered in Japan (72%) and the UK (at 71%), and substantially below average among business headquartered in the US (40%) and Switzerland (43%).

The Fair Tax Foundation’s pCbCR Resource Hub includes a running assessment of corporate tax transparency reports from around the world, as stipulated by countries implementing the EU pCbCR Directive. We have now sourced and analysed 190 corporate responses.

Previous analysis was focused on Romania, which implemented the pCbCR Directive much earlier than other EU member states.1 However, public country-by-country corporate income tax reports are now emerging in Croatia and Spain, who also operationalised the pCbCR Directive early.2

Whilst the majority of multinationals that are impacted by the EU pCbCR Directive have implemented these new tax transparency rules with integrity and courage, there is a substantial minority of business (especially those based in the United States and Switzerland) that have opted to do little or nothing.3

")

The gap between the corporate progressives and the corporate laggards has again widened since our previously reported analyses. As presented in June, July and October 2025. The overall level of solid compliance has fallen from 63% to 56% – it would seem that the first movers were generally more progressive than businesses who followed later.

Our latest analysis reveals that:

- More than half (56%) of corporate pCbCR reports are good, solid attempts to implement legislation driven by the EU pCbCR Directive.

- However, in 6% of instances, business have opted to confine disclosures to EU designated tax havens, and refuse to be transparent about their impact across EU Member States.

- Worse still, a third of parent companies (32%) will not share global CbCR data with their Romanian, Croatian or Spanish subsidiaries and are effectively refusing to implement the legislation. The proportion of US-business that opt for this ‘Single country only’ approach (48%) now exceeds the percentage that embrace pCbCR compliance solidly (40%). However, a quarter of the companies associated with ‘single country only’ filings pledge to file much more comprehensive reports in the near future.

The frequency of good application of the EU pCbCR requirements was substantially above average among business headquartered in Japan (72%) and the UK (at 71%). It was substantially lower than average among business headquartered in the US (40%) and Switzerland (43%).

The frequency of good application of the EU pCbCR requirements was substantially above average among business headquartered in Japan (72%) and the UK (at 71%). It was substantially lower than average among business headquartered in the US (40%) and Switzerland (43%).- A significant minority of business (12%) embraced the spirit as well as the letter of the legislation, and progressed full public country-by-country reporting and/or voluntarily progressed the EU pCbCR ahead of legislative requirements.

- The pharmaceuticals sector had a significantly below average rate of compliance: with just four of the twelve companies (33%) showing solid implementation of the directive, whilst five (50%) opted for the ‘Single country only’ option. The automotive and oil, gas & mining sectors also stood out as laggards. Conversely, the industrials sector demonstrated above average levels of compliance and responsibility, as did chemicals and communications.

- Multinationals filing pCbCR in Romania are now entering their second reporting second cycle. So far, there seems to be very little difference between the quality of returns between year one and year two.

- It is interesting to be able to discern which businesses have reduced their presence in Russia (defined by the EU as a tax haven) and which have still not.

- In Spain and Croatia, nearly half of companies producing ‘single country only’ filings pledge to do much more comprehensive reports in the near future, when year-end financial reporting and pcbcr analysis better aligns.

- CbC reports are increasingly machine readable – with xHTML datasets and connected machine-readable formatting, such as eXtensible Business Reporting Language (iXBRL) – as required by Commission Implementing Regulation (EU) 2024/2952 of 29 November 2024.

We hope to update this research on a regular basis, and it is freely available to all business that are involved in our Fair Tax Mark certification scheme. If you work in business and would like to engage with us on this work or access our pCbCR database, please reach out to [email protected]

For more detail and the very latest data, visit the Fair Tax Foundation pCbCR Resource Hub.

- The EU public Country-by-Country Reporting (pCbCR) Directive requires large multinational companies (with an annual consolidated turnover of at least €750m) that have a substantial presence in Europe to publicly share key financial information on their operations in each EU Member State and a designated list of tax havens. Multinationals (see our pCbCR Global Tracker for a list of EU and EEA States and the designated ‘tax havens’). In the main, the Directive will lead to major new corporate tax disclosures in 2026, based on 2025’s financial data. However, Romania opted to implement the EU Directive much earlier than other Member States, with data relating to 2023 starting to emerge at end 2024. An unintended consequence of this is that only multinationals with significant operations in Romania, but that are headquartered outside of the EU, are impacted – i.e., businesses with an ultimate parent entity in the US, Switzerland, Japan, the UK, etc.

- Of the 190 corporates analysed, 167 progressed filings in Romania, seven progressed filings in Spain and four progressed filings in Croatia. One progressed parallel filings in both Romania and Croatia and eleven multinationals released public CbC reports earlier than required in countries such as France and Denmark.

- The Fair Tax Foundation has conducted regular, comprehensive online searches to find these first EU pCbCR public reports and analysed them. There is no central repository of reports. We have identified 190 material corporate responses to date. Research was not as simple as might be hoped as the Romanian business register is not yet operational as a public repository of such information and there are no penalties in Romania for neglecting to implement the legislation as required. We have also yet to extract reports from wither the Croatian or Spanish business registers, albeit disclosure requirements in these countries are very recent. Which means, we suspect, that there are a large number of businesses who have simply opted to ‘ignore’ the legislation and act as though it doesn’t exist. This needs to be borne in mind in the analysis that follows. At the very least, all of the 190 companies identified has producing information on their website in connection with Romania’s, Croatia’s and Spain’s early implementation of the pCbCR Directive have acknowledged its existence in some way. Note: Note – all 190 assessed corporate responses are driven by either: i) mandatory capture of multinationals by Romania’s early implementation of the EU pCbCR Directive; or, ii) explicit, early voluntary implementation of the Directive by multinationals. Other businesses voluntarily already meet, or surpass the EU pCbCR requirements. Including a good number of Fair Tax Mark accredited businesses, such as Fortum (Finland), Iberdrola (Spain), Mace and SSE (UK) and Mundys (Italy). However, they have not been including in this analysis as they do not explicitly claim that their reporting currently meets the EU pCbCR standard