Welcome to our Public Country-by-Country Reporting (pCbCR) Resource Hub

Here we set out why and how multinational business should embrace tax transparency, together with the very latest news and analysis

Public Country-by-Country Reporting (pCbCR) of tax information by multinational enterprise is the hottest topic in financial reporting right now.

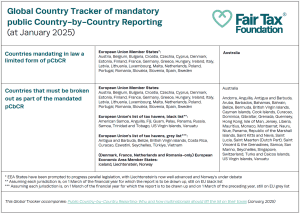

Driven by legislative developments in Europe and Australia, and accounting developments in the United States, the year 2026 will be a breakthrough year for corporate pCbCR – when there will be a cascade of corporate tax transparency from thousands of businesses, based on data from 2025 and accounting preparations undertaken in 2024. The focus is very much on corporate income tax, as explained in Why Corporate Income Tax is the most critical of all taxes.

Early adoption of EU legislation in Romania, Croatia and Spain has even seen large businesses with a substantial presence in these countries, and which have an ultimate parent entity outside of the EU, needing to take action from early 2025! Multinationals based in the likes of the United States, the United Kingdom, Japan and Switzerland have become the first wave of corporate income tax pCbCR pioneers.

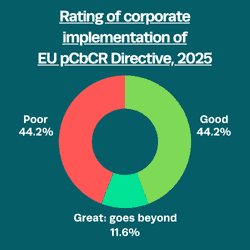

We have been tracking the first wave of tax transparency reports to emerge as a consequence of the EU pCbCR Directive, and publishing regular analysis of our findings to date. Most recently, analysis was provided 12th January 2026. This revealed that just over half (56%) of the 190 corporate tax transparency reports published by large multinationals in connection with the EU Public Country-by-Country Reporting (pCbCR) Directive are good, solid attempts to be open and honest. However, there are wide national variances. The frequency of good application of the EU pCbCR requirements was substantially above average among business headquartered in Japan (72%) and the UK (at 71%), and substantially below average among business headquartered in the US (40%) and Switzerland (43%).

We have been tracking the first wave of tax transparency reports to emerge as a consequence of the EU pCbCR Directive, and publishing regular analysis of our findings to date. Most recently, analysis was provided 12th January 2026. This revealed that just over half (56%) of the 190 corporate tax transparency reports published by large multinationals in connection with the EU Public Country-by-Country Reporting (pCbCR) Directive are good, solid attempts to be open and honest. However, there are wide national variances. The frequency of good application of the EU pCbCR requirements was substantially above average among business headquartered in Japan (72%) and the UK (at 71%), and substantially below average among business headquartered in the US (40%) and Switzerland (43%).

At the bottom of this page you will find our running macro-assessment of the raw numbers (as at 12th January 2026).

Paul Monaghan, Fair Tax Foundation, Chief Executive commented: “There is much to celebrate in our findings, but also causes for concern. The majority of multinationals that are impacted by the EU pCbCR Directive have implemented these new tax transparency rules with integrity and courage. Some have even taken the opportunity to go much further, and extend their reporting to all countries in which they operate and to other taxes. Others have opted to implement the directive earlier than required. On the other hand, many businesses, especially those based in the United States and Switzerland, have opted to do little or nothing. This is regrettable, not least as robust implementation of the EU pCbCR is sure to become a prominent key performance indicator of responsible tax conduct among investors and other stakeholders.”

Institutional investors, asset managers and ratings agencies are salivating at the prospect of accessing such data for the first time and being able to form a more rounded view of company tax conduct. Whilst firms engaging in higher levels of tax avoidance tend to be averse to disclosing CbC information, research has found that investors are rewarding increased transparency and tax-responsible behaviour via a lowering of the cost of equity capital.

The legislative and accounting developments are far from perfect, but they will raise the tax transparency bar considerably and serve as an embarkment point for those multinationals who rightly decide that they may as well go ‘all in’ and embrace full and complete pCbCR, as championed by the Fair Tax Mark.

Where mandatory pCbCR has already been introduced (e.g., in connection with large European banks and extractive industries), there is evidence of reduced use of tax havens, reduced profit shifting, increased effective tax rates and increased domestic tax revenue mobilisation.

Mandatory pCbCR would enable low- and lower middle-income countries to have access to large multinationals’ CbCR data for the first time – given the majority of these countries are currently locked out of global confidential information sharing systems.

Businesses that are Fair Tax Mark accredited are well placed to transition painlessly to a world where a step change in tax transparency is increasingly an expected, if not a mandatory requirement